The Huge Historical Impact of Type 1, 3-Cent Silvers

Although all Three Cent Silvers are unusual U.S. coins, Type 1 Three Cent Silvers were historically, legally, and physically different from Type 2 and Type 3 Three Cent Silvers.

The law that authorized Type 1 Three Cent Silvers led to a permanent change in the monetary order of the United States. In the United States, silver was never again regarded as money to the extent that it was before trimes were minted.

Three Cent Silvers are unlike Three Cent Nickels, which were minted from 1865 to 1889. Three Cent Nickels do not contain any silver and Three Cent Silvers do not contain any nickel.

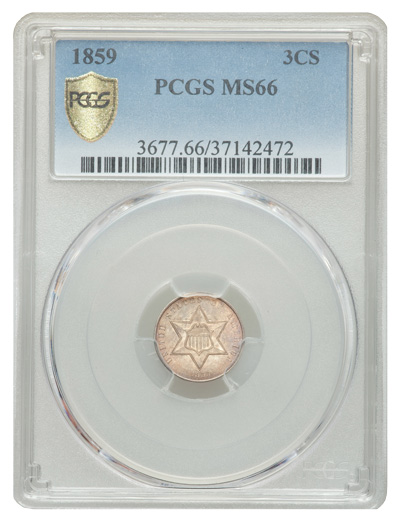

Type 1 Three Cent Silvers were minted from 1851 to 1853. Type 2 Three Cent Silvers were introduced in 1854, and the third type began in 1859. The distinctions between Type 2 and Type 3 Three Cent Silvers are not as significant as the differences between Type 1 and Type 2 coins.

On Type 2 Three Cent Silvers, the star on the obverse (front) is larger and additional elements were added to the reverse (back) design of Type 2 Three Cent Silvers. A branch with leaves was placed above and arrows were placed below the Roman numeral III, which was indicative of the denomination.

Type 3 coins are very much like Type 2 Three Cent Silvers, though there are noticeable differences. The outlines of the obverse star were modified. Moreover, the letters and numerals on the obverse are of different designs and sizes, plus their arrangement is very different from that on Type 2 trimes. Both Type 2 and Type 3 Three Cent Silvers were specified to be 90% silver and are of the same weight.

From 1794 to 1836, half dimes, dimes, quarters, half dollars and dollar coins were specified to be 1485/1664 silver (89.243%), though not all silver denominations were minted each year. Beginning in January 1837, a law required U.S. coins of silver denominations to be 90% silver in composition, a policy which remained in effect until 1964, with the exception of Type 1 Three Cent Silvers, which are 75% silver.

From 1794 to early 1853, the net weight in silver of U.S. silver coins was legally mandated to be 3.7125 grains of silver for every one cent of face value, 1/100 of a dollar. Type 1 Three Cent Silvers were the first exception.

A silver dollar was specified to contain 371.25 grains of silver (0.7734375 Troy ounce). A dime thus contained 37.125 grains of silver (about 0.077 Troy ounce) and a quarter contained 92.8125 grains (about 0.193 Troy ounce) of silver. Except Three Cent Silvers, the net silver weight in grains of each pre-1853 U.S. silver coin was the product of the respective face value (in cents) multiplied by 3.7125. Classic U.S. silver coins also contain copper.

Before the 1960s, the silver content of a U.S. silver coin was of tremendous importance to the general public, especially so in the 19th century. Grains were the pertinent standard measure of the 18th and 19th centuries. There are 480 grains in one Troy ounce, which remains the standard unit for silver and gold. One Troy ounce weighs 31.035 grams.

To be consistent with the Mint Act of 1792 and longstanding policy, a Type 1 Three Cent Silver (1851–53) coin should have contained 11.1375 grains of silver, three times 3.7125. To have been consistent with the Coinage Act of 1837, each Type 1 Three Cent Silver should have weighed 13.375 grains in total (0.02578125 Troy ounce) with 10% copper content, 1.3375 grains. The Type 1 Three Cent Silver was instead shockingly peculiar. It was indicative of a policy that sliced precedents and traditions. Indeed, it could have been credibly argued that Type 1 Three Cent Silvers were unconstitutional and dishonest.

In accordance with a then new law, each Type 1 Three Cent Silver was specified to weigh 12.375 grains and be 75% silver (rather than the 90% standard since 1837). The net silver content of each Type 1 Three Cent Silver was 9.28125 grains, way below 11.1375 grains and thus way below three cents worth of silver in terms of the official linkage of dollars to silver by the U.S. Treasury Department. Am I the only coin expert to point out that each Type 1 Three Cent Silver contained just 2.5 cents worth of silver?

In 1851, the U.S. Congress planned for Three Cent Silvers to be below par in silver content, and the president signed the pertinent new law on March 3, 1851. Politicians felt this measure was necessitated by the hoarding of U.S. silver coins by the general public. In other words, Type 1 Three Cent Silvers were deliberately planned such that they each contained just 2.5 cents worth of silver, a change in policy that would have been considered unthinkable or fraudulent before 1850.

Of course, economists, many businessmen, astute politicians, and savvy consumers all knew in 1851 that the government-set ratio of silver to U.S. dollars was temporarily or permanently in conflict with market realities. Nevertheless, as the rule was that one U.S. dollar was worth 371.25 grains of silver, the government was breaking its own rule and was shaking the monetary order

According to Neil Carothers (Fractional Money, NY: Wiley, 1930, p. 109), early in 1851, twenty half dimes, ten dimes, four quarters, or two half dollars were worth $1.035 in gold. In other words, U.S. silver coins were then worth more in gold than their face value in dollars.

During 1851 and 1852, U.S. silver coins were often set aside, exported or bartered, rather than spent. Although pertinent silver coins of the former Spanish Empire and successor societies in Latin America were legal tender until 1857, the U.S. Mint could not then practically buy many of them just by paying their U.S. money equivalents.

Also, Type 1 Three Cent Silvers were legal tender only for amounts up to thirty cents. In his widely acclaimed academic publications, Neil Carothers stated that the U.S. Treasury used government holdings of silver bullion to mint Three Cent Silvers and exchanged them for any U.S. silver or traditional Spanish silver coins. As one hundred Type 1 Three Cent Silvers contained substantially less silver than three silver dollars, six half dollars, or a dozen quarters, the U.S. Mint was profiting in 1851 and 1852 by exchanging Type 1 Three Cent Silvers for any U.S. silver coins already in circulation.

The law that allowed for Type 1 trimes set a precedent for further debasement of silver denominations, as the term debasement was understood before the 20th century, a government ordered reduction of the precious metal content of a coin type in production without a reduction in face value.

Although the introduction of Type 1 trimes alleviated the coin shortage, their effect was very limited. In 1851 and 1852, one U.S. dollar in gold continued to be worth notably more than one U.S. dollar in silver coins. For example, someone who traded ten half dollars for a half eagle ($5 gold coin) was losing money and the recipient of the ten half dollars was profiting. In 1851 and 1852, ten half dollars were worth more than $5 if traded for gold bullion!

The silver content of half dimes, dimes, quarters and half dollars (but not silver dollars) was reduced by law in 1853, and the role of silver in U.S. coinage became complicated. During 1851 and 1852, people were hoarding silver coins because gold discoveries in California had upset the market ratio of silver to gold, though the official government-fixed ratio (16:1) remained the same as this ratio of silver to gold was central to the whole U.S. monetary order.

U.S. citizens then thought and were told by politicians that the U.S. dollar was defined by specific quantities of silver and gold, bimetallism. Elected politicians were in a bind because a large increase in the supply of gold, through mining, caused the value of silver bullion in terms of gold to increase in market environments.

Silver dollars were exempt from the Coinage Act of 1853. For half dimes, dimes, quarters, and half dollars, the amount of silver for each cent of face value ($0.01) was reduced from 3.7125 grains to 3.456 grains. For example, the amount of silver in a newly minted quarter before 1853 was the product of 25 x 3.7125, 92.81 grains (0.1934 Troy ounce). Quarters struck after the Coinage Act of 1853 was implemented each contained 25 x 3.456 = 83.40 grains (0.180 Troy ounce) of silver.

Late in the 19th century, a leading historian of the U.S. Mint, David Watson, noted that the Coinage Act of 1853 reduced the value of new silver coins, except silver dollars, by 7%, and the new silver coins were legal tender only for amounts up to $5 in any one transaction. “No such antagonism to silver has been shown in the legislative history” of the United States before the Coinage Act of 1853, asserted Watson (History of American Coinage, NY & London: G. P. Putnam’s & Sons, 1899, p. 106). Actually, Watson’s point is not quite true, as the law in 1851 authorizing Type 1 Three Cent Silvers reduced the silver content in each per one cent in face value by one sixth (more than 16%) rather than by 7%.

With the introduction of Type 2 Three Cent Silvers in 1854, the composition was changed to 90% silver and 10% copper, from 75% silver and 25% copper. Type 1 Three Cent Silvers are the only U.S. coins that were specified to be 75% silver.

The silver content of Type 2 Three Cent Silvers (1854–58) was changed to be in line with the silver content per U.S. cent of face value of half dimes, dimes, quarters and half dollars, as stated in the Coinage Act of 1853. Each Type 2 Three Cent Silver was specified to contain 10.368 grains of silver (3 X 3.456), more than each Type 1 Three Cent Silver. While each Type 1 trime contained 2.5 cents of silver, each Type II trime contained about 2.79 cents worth of silver.

The Coinage Act of 1853 “denied to the holder of silver bullion the right to have his bullion coined into half-dollars, quarter-dollars, dimes, and half-dimes, and limited the coinage of these subsidiary coins to the pleasure of the Government,” cried Watson (p. 106)

Towards the end of the 19th century, J. Laurence Laughlin asserted that “in 1853 the actual use of silver as an unlimited legal tender equally with gold was decisively abandoned” ( https://tinyurl.com/History1853dollar). For around a half-century, from 1883 to 1933,Laughlin was one of the leading economists in the U.S. He refers to the Coinage Act of 1853 as causing “the real demonetization” of silver, even though it was not revealed by politicians to be so (Laughlin, The History of Bimetallism in the United States, NY: Appleton, 1895, p. 80).

While writing late in the 19th century, Laughlin and Watson both missed the

point that the Type 1 Three Cent Silver set the precedent for the

revolutionary reduction of the role of silver in the U.S. monetary order.

In 1851, most members of the U.S. Congress and much of the general public

found it to be constitutional, logical and ethical for a Type 1 Three Cent

Silver to contain only 2.5 cents worth of silver, according to the monetary

framework that had been in place since the Mint Act of 1792, It was the

introduction of the Type 1 Three Cent Silver that poked a large hole in the

monetary order and began the formation of a new reality in regard to the

meaning of a U.S. dollar.

Copyright ©2022 Greg Reynolds

Insightful10@gmail.com

Images courtesy of Heritage Auctions, HA.com.

Download the Greysheet app for access to pricing, news, events and your subscriptions.

Subscribe Now.

Subscribe to RQ Red Book Quarterly for the industry's most respected pricing and to read more articles just like this.

Visit these great CDN Sponsors

CDN Sponsors

Source: Greg Reynolds

More than 750 of Greg Reynolds’ articles about coins and related items have appeared in ten different publications. Reynolds has closely examined a tremendous number of rare, or conditionally rare, vintage U.S., British and Latin American coins. Furthermore, he has attended dozens of major coin auctions, including those of Eliasberg, Pittman, Newman, Gardner and Pogue Family. From the NLG, Reynolds has shared or won outright the annual award for ‘Best All-Around Portfolio’ a record seven times. Greg is available for private consultations and analyses, especially regarding rarities and auctions.

More than 750 of Greg Reynolds’ articles about coins and related items have appeared in ten different publications. Reynolds has closely examined a tremendous number of rare, or conditionally rare, vintage U.S., British and Latin American coins. Furthermore, he has attended dozens of major coin auctions, including those of Eliasberg, Pittman, Newman, Gardner and Pogue Family. From the NLG, Reynolds has shared or won outright the annual award for ‘Best All-Around Portfolio’ a record seven times. Greg is available for private consultations and analyses, especially regarding rarities and auctions.

Related Stories (powered by Greysheet News)

View all news

In this article Greg Reynolds analyzes the 1814 Capped Bust Half Dollar.

The Lusk set of Draped Bust quarters brought strong results.

The 1889-CC is the second scarcest business strike in the series.

Please sign in or register to leave a comment.

Your identity will be restricted to first name/last initial, or a user ID you create.

Comment

Comments